Policymakers and proponents of carbon capture and storage (CCS) as a means of decarbonising industry need to come up with a comprehensive plan, and not just focus on clusters, according to a new government-commissioned report.

Deep decarbonisation of UK industry is required to hit net zero and CCS, which is yet to be commercially proven at scale, is seen as a key tool. Yet to date, most studies and proposed business cases focus on industrial clusters close to offshore storage sites.

Element Energy’s review of CCS deployment at dispersed industrial sites looks at inland and isolated big emitters, such as cement, steel, ceramics and refineries. It sets out whether and how they could be decarbonised via CCS, and what the different options, such as pipelines or rail or road transport, might cost.

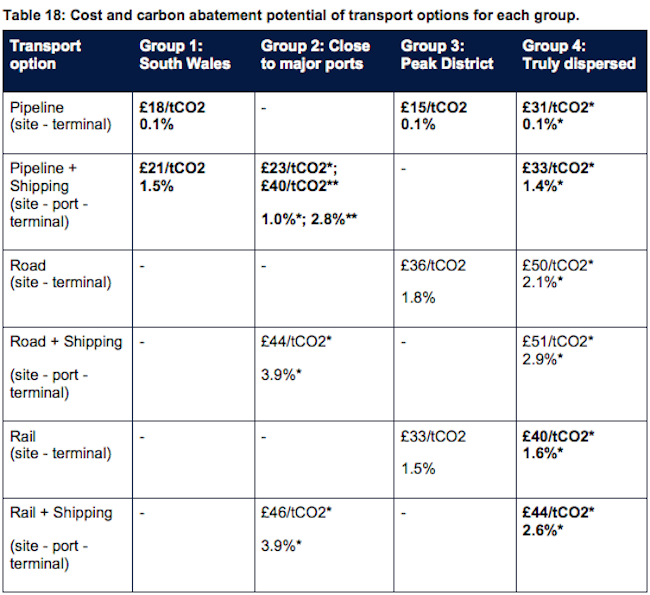

The report suggests there are 36 ‘dispersed’ industrial sites in the UK that may be suitable for CCS, collectively emitting almost 21 million tonnes of CO2. It grouped these into four types: those in South Wales; those close to major ports; those in the Peak District; and ‘truly dispersed’ sites.

In three of the four groups, Element Energy’s modelling suggests pipelines or a combination of pipelines and shipping are the lowest cost options for transporting the captured carbon. However, for the most dispersed sites it varied by individual site. Transport costs ranged from £15-£51/tCO2 depending on combinations modelled.

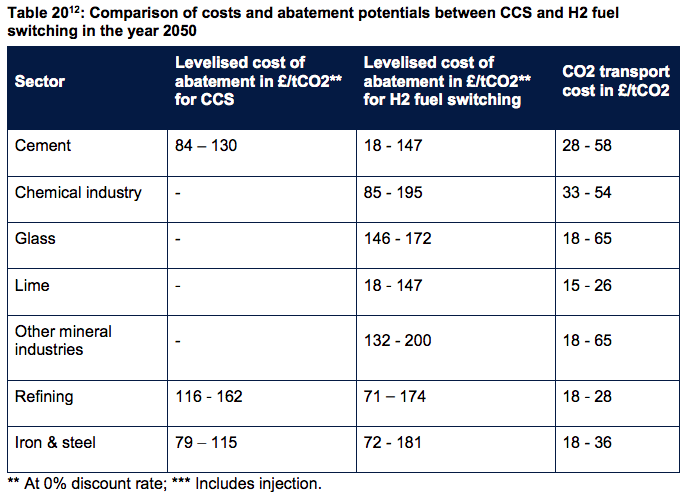

The analysis also weighed up other options, such as hydrogen switching as well as carbon capture and usage and storage, where the carbon is used in another product or process.

However, it cited product quality and equipment compliance concerns around hydrogen, plus “a general lack of technology readiness and a small market” for CCUS.

“In addition, one of the main technical considerations of CCS is the availability and cost of transport infrastructure for CO2. Hydrogen fuel switching would also encounter many of these challenges, as would CCU unless emitters and users are collocated, which for dispersed sites is more unlikely than for clusters,” states the report.

Element Energy also compared the abatement potential of hydrogen versus CCS, outlined in the table below.

Details here.

As we near 2050, all CO2 emitting sources must be phased out, one of these is carbon capture which under the best conditions is only up to 95% efficient, and CO2 storage is expensive as this report shows, as well as the cost of pumping the CO2 at high pressure into deep geological formations. Industries that use CC and storage (CCS) must replace it with other technologies by 2050 that do not emit even small amounts of CO2. The steel industry can convert smelting with hydrogen (H2) instead of carbon, refineries and petrochemicals can either produce the millions of tons of H2 that they need each year by electrolysis of water or by cracking methane directly into H2 and graphite with the Hazer process.