Europe added a record 13.5GW / 26.4GWh of electrochemical storage in 2025, surpassing 100GW of installed storage capacity across all technologies. While deployment continues to accelerate, significant opportunities remain across every European market as electrification and renewable energy continue to expand.

The latest edition of the European Market Monitor on Energy Storage (EMMES), published today by LCP Delta and Energy Storage Europe, reveals that Europe’s energy storage market reached another major milestone in 2025, with total installed storage capacity surpassing 100GW for the first time and reaching 102.7GW.

Marking its tenth year, the report provides a comprehensive overview of energy storage capacity across EU countries, Great Britain, Switzerland and Norway, covering installed capacity to date, projects due online in 2026, and forecasts through to 2030.

Energy storage has overtaken nuclear capacity, while the number of operating nuclear reactors has been steadily declining. The shutdown of nuclear plants in Germany has been the biggest contributor to this, removing around 11GW of capacity, while Great Britain and Belgium have also decommissioned a significant number of reactors since 2016. However, recent decisions in both countries have sparked a renewed push for nuclear energy.

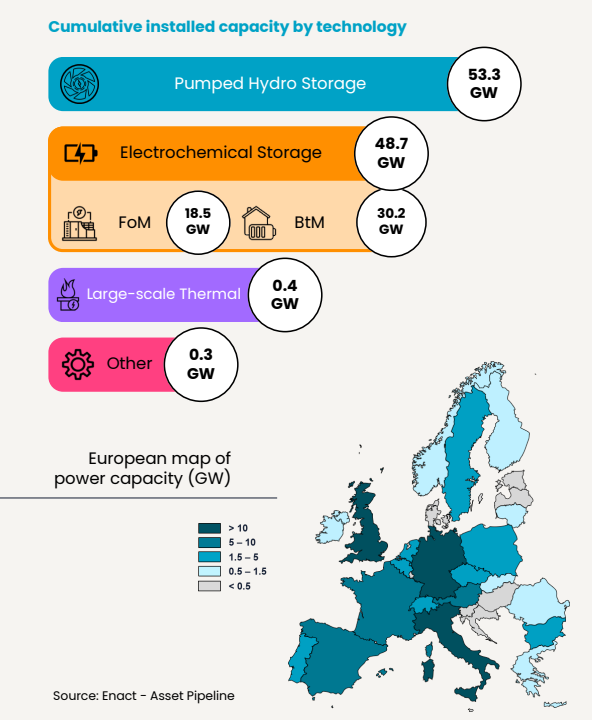

Behind-the-meter (BtM) storage has been key to this progress, with 30.2GW / 46.2GWh of electrochemical capacity installed by the end of 2025, led by Germany, Italy, the Netherlands, Austria and Great Britain. The experts highlight that growth is being driven by solar-plus-storage adoption, the rollout of dynamic electricity tariffs, increasing electrification of homes and businesses, and participation in flexibility markets.

Front-of-the-meter battery storage (FoM) has also expanded, reaching 18.5GW / 34.4GWh by the end of 2025. Momentum has been significant in countries with established capacity markets, including Great Britain, Italy, Poland and Belgium, as well as those with dedicated large scale storage support schemes, such as Italy, Bulgaria, Poland and Spain.

Significant growth potential remains across Europe

Despite record levels, the report finds that no European market has yet reached its full storage potential. As renewable energy deployment accelerates and electricity demand continues to grow through electrification of transport, heating and industry, the need for storage is expected to increase substantially by the end of the decade.

Compared with last year’s outlook, EMMES 10.0 raises expectations for utility-scale battery deployment by 25%, reflecting stronger market fundamentals, growing project pipelines and increasing confidence in the role of storage within Europe’s future energy system.

Looking ahead to 2030, Germany and Italy will dominate total installed BtM capacity, followed by the Netherlands, Great Britain, and Austria. For FoM capacity, Great Britain and Italy are expected to lead, with Germany, Poland, and Spain following behind. As energy storage continues to scale, ensuring that projects can connect efficiently and participate fairly in electricity markets will become increasingly important. The report highlights the need for market frameworks that properly value storage, alongside grid planning and connection processes capable of supporting continued growth.

Silvestros Vlachopoulos, Energy Storage Research Manager at LCP Delta and lead author, said, “The continued growth in energy storage shows that the industry recognises its value and benefits. While this momentum is encouraging, the focus must now shift to keeping pace with rising demand.

“Our analysis indicates that energy storage will continue to expand through to 2030, providing a clearer picture of where additional support is needed to ensure its success. Grid capacity is also becoming an increasingly important part of the conversation.”

Jacopo Tosoni, Energy Storage Europe Deputy Secretary-General and Head of Policy, said, “The European storage market is entering a new phase. Reaching over 100GW of installed storage capacity is a remarkable achievement, but the greatest opportunity still lies ahead. No European country has yet reached its storage potential, while electrification, renewable deployment, and system needs continue to grow.

“To unlock this growth, Europe must ensure storage can compete on a level playing field across electricity markets. Clear investment signals, technology-neutral market design, faster permitting and grid connections, and better access to flexibility stability, and capacity mechanisms will be key to delivering the storage volumes needed for Europe’s future energy system.”