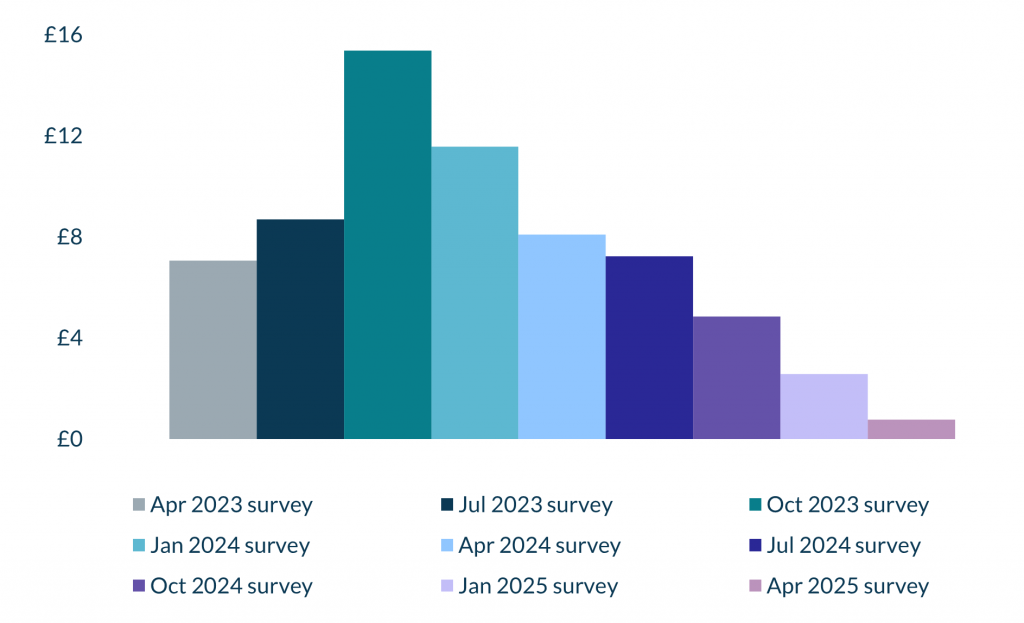

The future of Renewable Energy Guarantees of Origin (REGOs) is facing growing uncertainty as prices collapse and confidence in the system wanes. According to Cornwall Insight’s latest Green Certificates Survey1, prices for REGOs – certificates bought by suppliers to demonstrate electricity was generated from renewable sources – have dropped by 70% in just three months, falling for the sixth consecutive quarter. With high supply and lower demand seeing costs fall.

The dramatic drop in price, from an average of £2.56 in January to just £0.77 in April for the 2024–25 Fuel Mix Disclosure period, is being driven by a surge in renewable energy supply. There is also waning demand, with a shift among corporates toward alternative decarbonisation methods such as power purchase agreements (PPAs), and increasing questions over whether REGOs are truly helping the drive towards decarbonisation.

REGOs are issued by Ofgem to renewable electricity generators for each megawatt hour (MWh) of renewable electricity they produce. Suppliers buy these certificates to demonstrate that the electricity they provide to customers is backed by renewable generation. But, because all electricity mixes once it enters the grid, REGOs have drawn criticism from some quarters as a form of ‘greenwashing’.

Some major suppliers in the UK have also questioned the effectiveness of REGOs, with OVO

announcing in 2023 that it would stop purchasing them entirely. Whether other suppliers will follow suit, and what reforms may ultimately emerge, could reshape the role of REGOs in the UK’s decarbonisation journey.

The sharp drop in prices follows a period of historically high REGO prices in 2023, which reached average highs of over £15 per certificate. This was driven by limited new capacity in the Government’s renewables auction – Contract for Difference (CfD) – allocation rounds, delays to existing renewable projects, and additional demand triggered by suppliers no longer being able to use EU Guarantees of Origin.

With prices falling to levels last seen in 2021, the question is what comes next. The UK Government held a call for evidence on REGOs in 2021 and published a summary of responses in 2023 but has yet to set out a clear path for reform. A new workstream on greenwashing and consumer transparency is expected to begin later this year, as part of the ongoing Review of Electricity Market Arrangements (REMA). However, some in the industry have said this is not enough, and more clarity is needed on the future of REGOs.

There are some potential changes on an international scale which could dampen the use of REGOs further, for example the global group for greenhouse gas emissions – Greenhouse Gas Protocol – is launching a review of how global organisations report electricity-related emissions, including the use of renewable certificates such as REGOs. Asking whether they truly lead to additional renewable energy generation, and could potentially slow down the overall reduction of global emission.

Cornwall Insight’s Green Certificates Survey gathers insight from sellers, buyers, brokers, and generators to track market sentiment and trends in the REGO market.

Figure 1: Average REGO Prices (£/MWh) for Fuel Mix Disclosure Period 2024-25

Source: Cornwall Insight – Green Certificates Survey

Dr Matthew Chadwick, Lead Research Analyst, at Cornwall Insight, “We’re not just seeing prices tumble, we’re seeing confidence in the REGO system itself start to crack. As renewable supply surges and buyers seek alternatives, these certificates are losing their position as the default way to demonstrate green credentials. What was once a relatively niche market is now under national scrutiny, and its future hangs in the balance.

“As prices continue to fall and questions mount, there’s growing unease about whether REGOs still serve their purpose. Are they genuinely helping to drive decarbonisation, or simply offering a convenient green label? Without meaningful reform – or potentially a new approach altogether – there’s a real risk that trust in the system will erode further.”

1. 23 individuals from 20 distinct organisations participated: 22 participants traded in REGOs, 15 identified their role primarily as sellers; 4 as buyers; and 2 as brokers/traders, and one as a REGO producer with an oversight of trading.