Firms planning gigawatts of battery storage are weighing up new derating factors published by government that will make short duration assets less valuable in the capacity market.

Firms planning gigawatts of battery storage are weighing up new derating factors published by government that will make short duration assets less valuable in the capacity market.

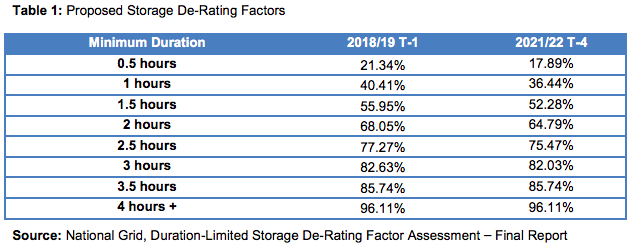

Batteries that can deliver for only half an hour will be rated at around a fifth of their maximum output while assets that can discharge for four hours will receive the same derating factor as pumped hydro (96%).

The changes follow concerns by Scottish Power, which owns a lot of pumped hydro, that batteries should not be treated on the same footing.

The capacity market is intended to improve security of supply over winter. Auctions run one year ahead of delivery (called T-1) and four years ahead (T-4).

Companies building new power generation assets can bid for long-term contracts of up to 15 years in return for guaranteeing to provide power over the winter peak. There are also short-term contracts available for existing generation of all types – from big power stations to small engines and demand-side response.

In future, there may also be scope for unsubsidised renewables to bid in to the market, with Ofgem set to consult in spring on how that might work.

Capacity market costs are added to energy bills.

Bankable revenue

For batteries, and other forms of generation, securing long-term contracts is important because it provides a small but ‘bankable’ part of the revenue stream required to make batteries financeable. Much of the other revenues batteries can try to accrue are merchant, or short-duration contracts.

Battery developers planning to build assets with shorter durations will now be bidding for less revenue, if they decide to bid.

However, government said it had to ensure that it was not over-rewarding assets unable to provide cover for longer duration outages. National Grid analysis suggested the mean stress event duration is around two hours, but that most are under four hours.

The new derating factors, which apply going forward but not to existing CM contracts, reflect that requirement, said the department for business, energy and industrial strategy (Beis).

Adjust volume

Of around 27GW of new potential new build capacity prequalified for the T-4 auction, around 4.8GW is new battery storage.

Storage developers must now carefully consider whether to build longer duration batteries or drop out, given the overall prequalifying volume of generation is around 30GW above the government’s 50.5GW target. That may suggest a low clearing price may be on the cards if coal stations decide that staying open for four more years is worth their while.

Just over 2GW of storage also prequalified for the T-1 auction, which will have to compete with existing coal and gas plant.

While some storage developers may lament the derating factors being published after auction pre-qualification results, Beis had served warning in July, and others believe government is taking a prudent approach.

UK Power Reserve has prequalified some 600MW of gas and 400MW of batteries within the auctions.

The firm’s director of policy and regulation, Michael Jenner, said derating was “absolutely appropriate” and does not change the firm’s “bullish outlook” for UK distributed gas generation and battery storage.

“If you are looking to design a market to deal with a stress event, you want to reward assets commensurate with their ability to help reduce those stress events,” he told The Energyst.

“So derating of shorter term batteries is absolutely appropriate. It will make the market think carefully about options – the incentive is now there for investors to think about building longer duration storage assets.”

However, Jenner suggested derating factors could lead to fewer battery storage firms winning contracts than last year’s 500MW.

“Each investor has to make its own decision. But I would expect this to have a significant effect on bidding prices. Without derating, we would have seen a lot more batteries coming through – with the derating factor applied, we expect to see a much reduced battery play.”

While the auction outcome cannot be predicted, Jenner said he would “not be surprised if we saw fewer batteries win contracts than we saw last year.”

While some developers may “take it on the chin”, derating factors “could push a lot, if not most of it, out of the auction,” added Jenner.

“We will be looking carefully at what this means for us in next year’s auction but it doesn’t change our ambitious growth plans for battery storage in the UK, nor our positive view for the development of the industry as a whole,” he said.

See the CM register here, and the government’s battery storage derating consultation response here.

Industry reaction

Georgina Penfold, CEO, Electricity Storage Network:

“The changes to the derating factors for storage is significant, as it alters the business model for many projects depending on the relative power / energy ratios of the storage system. Inevitably there will be winners and losers. However, these changes were foreseeable. It is indicative of the fact that storage is becoming a mature technology.

The Government maintains that it is committed to the continued deployment of storage, and we are pleased to continue to work with them to promote appropriate development of storage assets both behind the meter and for system resilience.”

Frank Gordon, policy manager at the Renewable Energy Association:

“The Capacity Market is an ever more crucial mechanism for delivering battery projects, which underpin the additional electricity system flexibility that is so urgently needed in the UK.

“The changes unveiled today are slightly less drastic than those first proposed but could make it harder for a number of battery storage projects to compete. Storage projects over four hours duration, such as flow batteries that can hold power for longer lengths, will see no change from the decision.

“One cannot forget that this is one of many recent changes that are undermining the growth of this sector. Recent revisions to “embedded generation” payments slashed the support that small-scale, distributed generation receives and there could be more pain for the sector in future grid payments reform. Considering the Government research and development funding going towards batteries at the moment and the drive to encourage future battery manufacturing it seems strange to undermine the development of a battery storage market.

“The timing of these changes is our main criticism however. As they are being applied in the midst of an on-going auction process it akin to changing the rules of a football match at half-time.”

Scott McGregor, CEO, RedT:

“‘Derating’ is a negative word. But RedT will get the full rating of 96%, because our flow machines are long duration energy systems. So we think the announcement is great news. The only guarantee that anybody has in this market is that policy will change. That makes it crucial for storage platforms to be flexible.”

Alastair Martin, chief strategy officer, Flexitricity:

“I think National Grid adopted a good approach to the question they had been set. Their analysis method always struck me as the right one to apply to that problem. I’m not convinced it was the right question, however.

“The Capacity Market was intended to be additional to other revenue sources, which could include energy, ancillary services, locational support, and so on. Since those other revenue sources reward different capabilities in different ways, market forces will shape the capabilities which people will build, and the CM can be technology-neutral. That, at least, was the idea.

“For batteries, CM revenue alone cannot fund development, so they rely on contracts like frequency response to form part of the revenue stack. There’s only so much half-hour-duration frequency response that National Grid can use. According to CM design principles, market forces should restrict the volume of half-hour batteries without anyone intervening in the CM.

“There are other things beyond duration that affect what effect capacity has on system security, like location, speed, inertia and reactive power capabilities. For example, when it’s very windy, other generation in Scotland can’t help secure supplies in England and Wales, because if it’s turned up, then the wind has to be turned down. If BEIS is removing technology neutrality from the CM, then it should be considering all of those other factors. As it is, it has cherry-picked the problem it is trying to solve, lost faith in the market on that score only, and sent a baffling message to the industry.

“The other likely outcome is that hybrid storage/peaker sites could become the norm. A number of developers are already pursuing this variation – by pairing short-run batteries with engines, you get near-instant response coupled with potentially unlimited duration. As a means of arbitraging renewables, it’s not as good as true long-range storage would be, because once the battery is exhausted, the site becomes a peaking station with no heat recovery, and we already have lots of those. So the hybrid role is still subject to market-force restrictions.

“I’m not seeing much that would suggest a breakthrough on long-range storage is imminent. There are encouraging signs, but those are coming from technology developers, not the CM.

“On the auction volumes, between existing generation and proven DSR, there’s 7.6GW in the T-1 auction. Another 6.5GW is available from unproven DSR and new-build generation. So the available volume dwarfs the requirement. Whether or not that means a price crash depends largely on how serious the bidders are. We can draw obvious inferences about short-run battery projects, but beyond that, pre-match analysis won’t tell us how this is going to turn out.

“On the T-4, the register looks in so many ways like previous pre-auction registers. Existing generation and proven DSR can meet all of the volume requirement. Whether the auction gets into new-build territory still depends on how existing stations view their energy market opportunities beyond 2021. Up to now, existing generators have been bullish.

“New build CCGTs have remained locked out partly because of this, and partly because new-build peakers treat energy market revenue very differently. Given other recent developments on network charging, the peakers might alter their tactics. But little has changed for the existing generators other than 2025 getting closer.”

Related stories:

Shifting the balance of power: New, free demand-side response report

Government plans rule changes for storage and DSR in capacity market

Scottish Power calls for rule changes for battery storage in capacity market

Half of small generators ‘could give up capacity market contracts’ after Triad cuts

Businesses ‘shutting down from 4-7pm due to peak power costs

Capacity market ‘buying the wrong stuff because it’s joined up with nothing’

Energy storage to be reclassified in Electricity Act

National Grid slashes long-term estimates for battery storage

Swindon Council plans 50MW battery storage plant

Eelpower commissions 10MW battery, plans 150MW

Battery storage: Where’s the smart money?

Energy storage ‘will wipe out’ battery storage

Battery storage to push frequency response revenues down STOR’s path?

National Grid confirms cull of frequency response products

Aurora: Battery storage, DSR and peaking plant to hit 25GW

Marks & Spencer mulls battery storage investment

Centrica to use council’s 3MW battery storage unit to balance local and national grids

Centrica: Floodgates on battery storage investment to open in 2017

Battery storage: Finance a challenge but businesses predict 3-7 year paybacks

As solar generation makes history, National Grid starts to feel the burn

UK Power Networks receives 12GW of storage applications

Limejump and Anesco partner to connect 185MW of capacity market battery storage

UK Power Networks outlines smart grid plans

UKPN sees battery boom, outlines DSR plans

Government sets out smart grid vision

National Grid adds 500MW of flexibility in 2016, more to come

As solar subsidies wane, investors plan 2.3GW of battery storage projects

Vattenfall to build 22MW battery storage plant at south Wales windfarm

VLC Energy to connect 50MW of battery storage in 2017 after EFR contract win

Greg Clark calls for carmakers and energy firms to deliver battery storage

More than half of I&C firms mulling energy storage investment

Capacity market too low for large gas, but gigawatts of DSR, batteries and CHP win contracts

Battery storage: positive outlook?

National Grid must provide a plan for battery market, says SmartestEnergy

Who needs an EFR contract? Somerset solar site installs ‘grid scale’ Tesla battery

Ofgem: Energy flexibility will become more valuable than energy efficiency

National Grid says UK will miss 2020 targets, predicts big battery future

Nissan: Carmaker signals roadmap to energy services company

Flexitricity chief: UK has enough spare power electrify every car on the road

Government finds £20m for vehicle to grid development

Shifting the balance of power: New, free demand-side response report

Follow us at @EnergystMedia. For regular bulletins, sign up for the free newsletter.